Official Florida Sales Tax Template

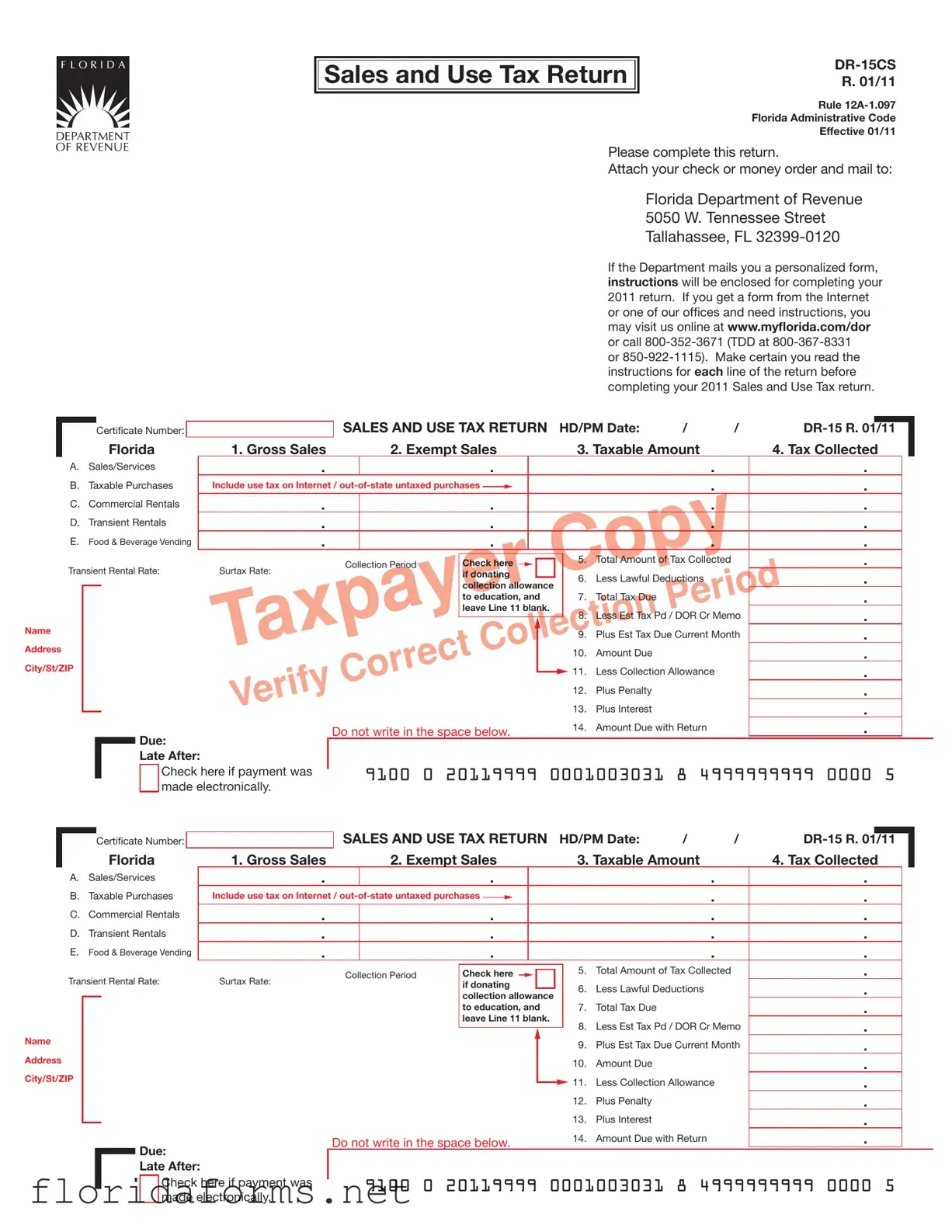

Navigating the intricacies of the Florida Sales Tax Form, officially known as the Sales and Use Tax Return DR-15CS, requires understanding its function and impact on businesses within the state. Effective from January 2011, this form plays a critical role in the administration of sales tax, serving as a detailed report that businesses must submit to account for their taxable sales, exempt sales, and ultimately calculate the tax due. It's not merely about reporting the tax collected from sales or services; it also extends to taxable purchases including those made out-of-state or over the internet that were not taxed, commercial and transient rentals, and even vending machine sales. Aside from calculating the total tax due, the form offers businesses the option to participate in socially responsible acts like donating a part of their collection allowance to education. Delving deeper, the form addresses the discretionary sales surtax, which varies by county, affecting how much tax is collected on sales depending on the location of the transaction. This is complemented by guidelines for handling transactions exempt from this surtax or those subject to a different rate. Moreover, it covers potential deductions and credits, such as those for enterprise zone job creation, that can impact the total tax liability. Penalties for fraudulent or incorrect filing underscore the legal responsibility businesses have in accurately reporting their sales and taxes. Positioned as a comprehensive tool, the form embodies the state's effort to regulate and collect sales taxes while offering businesses a structured means to comply with tax laws.

Example - Florida Sales Tax Form

Sales and Use Tax Return

Sales and Use Tax Return

R. 01/11

Rule

Florida Administrative Code

Effective 01/11

Please complete this return.

Attach your check or money order and mail to:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Florida Department of Revenue |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5050 W. Tennessee Street |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tallahassee, FL |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

If the Department mails you a personalized form, |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

instructions will be enclosed for completing your |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2011 return. If you get a form from the Internet |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

or one of our ofices and need instructions, you |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

may visit us online at www.mylorida.com/dor |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

or call |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

or |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

instructions for each line of the return before |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

completing your 2011 Sales and Use Tax return. |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

SALES AND USE TAX RETURN |

HD/PM Date: |

/ |

/ |

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

Certiicate Number: |

|

|

|

|

|

|||||||||||||||||||||||

|

|

|

|

|

Florida |

1. Gross Sales |

|

|

2. Exempt Sales |

|

|

3. Taxable Amount |

|

4. Tax Collected |

|

|

||||||||||||||||

|

|

A. |

Sales/Services |

|

. |

|

|

|

. |

|

|

|

|

|

|

|

|

|

. |

|

. |

|

|

|

|

|||||||

|

|

B. |

Taxable Purchases |

|

Include use tax on Internet / |

|

|

|

|

|

|

|

|

|

|

. |

|

. |

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

C. |

Commercial Rentals |

|

. |

|

|

|

. |

|

|

|

|

|

|

|

|

|

. |

|

. |

|

|

|

|

|||||||

|

|

D. |

Transient Rentals |

|

. |

|

|

|

. |

|

|

|

|

|

|

|

|

|

. |

|

. |

|

|

|

|

|||||||

|

|

E. |

Food & Beverage Vending |

|

. |

|

|

|

. |

|

|

|

|

|

|

|

|

|

. |

|

. |

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Amount of Tax Collected |

|

. |

|

|

|

|

|||||||

|

|

Transient Rental Rate: |

Surtax Rate: |

|

Collection Period |

Check here |

|

|

|

|

|

5. |

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

|

|

|

|

if donating |

|

|

|

6. |

Less Lawful Deductions |

|

. |

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

collection allowance |

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

to education, and |

|

7. |

Total Tax Due |

|

|

. |

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

leave Line 11 blank. |

|

|

|

|

|

|

|

|

|

|

|

||||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8. Less Est Tax Pd / DOR Cr Memo |

. |

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9. Plus Est Tax Due Current Month |

. |

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10. |

Amount Due |

|

|

. |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

City/St/ZIP |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

11. |

Less Collection Allowance |

|

. |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12. |

Plus Penalty |

|

|

. |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13. |

Plus Interest |

|

|

. |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

Due: |

|

Do not write in the space below. |

14. |

Amount Due with Return |

|

. |

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

Late After: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

Check here if payment was |

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

9100 0 20119999 0001003031 8 4999999999 0000 5 |

|

|

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

made electronically. |

|

SALES AND USE TAX RETURN |

HD/PM Date: |

/ |

/ |

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

Certiicate Number: |

|

|

|

|

|

|||||||||||||||||||||||

|

|

|

|

|

Florida |

1. Gross Sales |

|

|

2. Exempt Sales |

|

|

3. Taxable Amount |

|

4. Tax Collected |

|

|

||||||||||||||||

|

|

A. |

Sales/Services |

|

. |

|

|

|

. |

|

|

|

|

|

|

|

|

|

. |

|

. |

|

|

|

|

|||||||

|

|

B. |

Taxable Purchases |

|

Include use tax on Internet / |

|

|

|

|

|

|

|

. |

|

. |

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

C. |

Commercial Rentals |

|

. |

|

|

|

. |

|

|

|

|

|

|

|

|

|

. |

|

. |

|

|

|

|

|||||||

|

|

D. |

Transient Rentals |

|

. |

|

|

|

. |

|

|

|

|

|

|

|

|

|

. |

|

. |

|

|

|

|

|||||||

|

|

E. |

Food & Beverage Vending |

|

. |

|

|

|

. |

|

|

|

|

|

|

|

|

|

. |

|

. |

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Amount of Tax Collected |

|

. |

|

|

|

|

||||||||

|

|

Transient Rental Rate: |

Surtax Rate: |

|

Collection Period |

Check here |

|

|

|

|

5. |

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||

|

|

|

|

|

if donating |

|

|

6. |

Less Lawful Deductions |

|

. |

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

collection allowance |

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

to education, and |

|

7. |

Total Tax Due |

|

|

. |

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

leave Line 11 blank. |

|

|

|

|

|

|

|

|

|

|

|

||||||

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8. Less Est Tax Pd / DOR Cr Memo |

. |

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9. Plus Est Tax Due Current Month |

. |

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10. |

Amount Due |

|

|

. |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

City/St/ZIP |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

11. |

Less Collection Allowance |

|

. |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12. |

Plus Penalty |

|

|

. |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13. |

Plus Interest |

|

|

. |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

Due: |

|

Do not write in the space below. |

14. |

Amount Due with Return |

|

. |

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

Late After: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

Check here if payment was |

|

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|

9100 0 20119999 0001003031 8 4999999999 0000 5 |

|

|

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

made electronically. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Proper Collection of Tax: Florida’s general sales tax rate is 6 percent; however, there is an established “bracket system” for calculating the tax due when any part of each total taxable sale is less than a whole dollar amount. Other rates may also apply. See instructions.

Discretionary Sales Surtax: Most counties levy a discretionary sales surtax on most transactions subject to sales and use tax. These taxes are distributed to local governments throughout the state. The amount of money distributed is based on how you complete your tax return, especially the lines on the back of the return. Dealers should impose discretionary sales surtax on taxable sales when delivery or use occurs in a county that imposes surtax. Please see Form

Fraud Penalties: There are speciic penalties imposed for fraud, fraudulent claim of exemption, failure to collect and pay over, or an attempt to evade or defeat the sales tax. Please see the instructions for detailed information regarding the penalties, ines, and punishments for certain sales tax offenses.

Under penalties of perjury, I declare that I have read this return and the facts stated in it are true (sections 92.525(2), 212.12, and 837.06, Florida Statutes).

Signature of Taxpayer |

Date |

Signature of Preparer |

Date |

( ___________ ) ____________________________________________ |

|

( ___________ ) ____________________________________________ |

|

Telephone Number |

|

Telephone Number |

|

Discretionary Sales Surtax ( Lines 15(a) through 15(d) )

15(a). |

Exempt Amount of Items Over $5,000 (included in Column 3) |

15(a). _________________________________ |

15(b). |

Other Taxable Amounts NOT Subject to Surtax (included in Column 3) |

15(b). _________________________________ |

15(c). |

Amounts Subject to Surtax at a Rate Different Than Your County Surtax Rate (included in Column 3) |

15(c). _________________________________ |

15(d). |

Total Amount of Discretionary Sales Surtax Collected (included in Column 4) |

15(d). _________________________________ |

16. |

Total Enterprise Zone Jobs Credits (included in Line 6) |

16. _________________________________ |

17. |

Taxable Sales/Untaxed Purchases of Electric Power or Energy — 7% Rate (included in Line A) |

17. _________________________________ |

18. |

Taxable Sales/Untaxed Purchases of Dyed Diesel Fuel — 6% Rate (included in Line A) |

18. _________________________________ |

19. |

Taxable Sales from Amusement Machines (included in Line A) |

19. _________________________________ |

20. |

Rural and/or Urban High Crime Area Job Tax Credits |

20. _________________________________ |

21. |

Other Authorized Credits |

21. _________________________________ |

Under penalties of perjury, I declare that I have read this return and the facts stated in it are true (sections 92.525(2), 212.12, and 837.06, Florida Statutes).

Signature of Taxpayer |

Date |

Signature of Preparer |

Date |

( ___________ ) ____________________________________________ |

|

( ___________ ) ____________________________________________ |

|

Telephone Number |

|

Telephone Number |

|

Discretionary Sales Surtax ( Lines 15(a) through 15(d) )

15(a). |

Exempt Amount of Items Over $5,000 (included in Column 3) |

15(a). _________________________________ |

15(b). |

Other Taxable Amounts NOT Subject to Surtax (included in Column 3) |

15(b). _________________________________ |

15(c). |

Amounts Subject to Surtax at a Rate Different Than Your County Surtax Rate (included in Column 3) |

15(c). _________________________________ |

15(d). |

Total Amount of Discretionary Sales Surtax Collected (included in Column 4) |

15(d). _________________________________ |

16. |

Total Enterprise Zone Jobs Credits (included in Line 6) |

16. _________________________________ |

17. |

Taxable Sales/Untaxed Purchases of Electric Power or Energy — 7% Rate (included in Line A) |

17. _________________________________ |

18. |

Taxable Sales/Untaxed Purchases of Dyed Diesel Fuel — 6% Rate (included in Line A) |

18. _________________________________ |

19. |

Taxable Sales from Amusement Machines (included in Line A) |

19. _________________________________ |

20. |

Rural and/or Urban High Crime Area Job Tax Credits |

20. _________________________________ |

21. |

Other Authorized Credits |

21. _________________________________ |

File Specifications

| Fact | Detail |

|---|---|

| Form Identification | Sales and Use Tax Return DR-15CS R. 01/11 |

| Governing Rules | Rule 12A-1.097, Florida Administrative Code, Effective 01/11 |

| Submission Address | Florida Department of Revenue, 5050 W. Tennessee Street, Tallahassee, FL 32399-0120 |

| Instruction Availability | Instructions can be found online at www.myflorida.com/dor or by calling 800-352-3671 |

| Form Sections | Includes Gross Sales, Exempt Sales, Taxable Amount, Tax Collected, Deductions, Tax Due, Penalties, and Interest |

| Bracket System for Tax Calculation | Applies when part of a taxable sale is less than a whole dollar amount |

| Discretionary Sales Surtax | Subject to most transactions and varies by county. Form DR-15DSS provides surtax rates. |

| Fraud Penalties | Includes specific penalties for fraud, exemption claim fraud, failure to pay over, or attempting to evade sales tax |

Instructions on Filling in Florida Sales Tax

Filing a sales tax return in Florida can seem daunting, but with concise steps, the process becomes straightforward. Once the Florida Department of Revenue receives your completed Sales and Use Tax Return form, your business will be compliant with state tax regulations for the period. Remember to gather all necessary documents regarding your sales, exempt sales, and taxable purchases before starting. Pay special attention to accurately reporting surtaxes as these can vary by county and affect the total amount due. Here's how to fill out the form correctly:

- Enter the date of your report in the HD/PM Date field.

- Fill in your Certificate Number as it appears on your records.

- Report your total Gross Sales in section 1.

- Detail any Exempt Sales in section 2.

- Calculate and enter the Taxable Amount in section 3.

- Under section 4, break down the Tax Collected into categories: A. Sales/Services, B. Taxable Purchases, C. Commercial Rentals, D. Transient Rentals, and E. Food & Beverage Vending. Then, add these to report the Total Amount of Tax Collected.

- If applicable, check the box in section 5 to donate your collection allowance to education.

- List any Lawful Deductions in section 6.

- Calculate the Total Tax Due and enter this amount in section 7.

- Subtract any Estimated Tax Paid or DOR Credit Memo in section 8.

- Add any Estimated Tax Due for the Current Month in section 9.

- Enter the Amount Due in section 10.

- If applicable, subtract the Collection Allowance in section 11.

- Include any penalties in section 12 and any interest in section 13.

- Calculate the total Amount Due with Return, taking into account any electronic payments, in section 14.

- For the Discretionary Sales Surtax sections (15(a) through 15(d)), properly allocate exempt sales over $5,000, other taxable amounts not subject to surtax, amounts subject to a different surtax rate, and the total discretionary sales surtax collected.

- Enter any Enterprise Zone Jobs Credits in section 16.

- Report specific taxable sales or untaxed purchases for items like electric power or energy, dyed diesel fuel, and amusement machines in sections 17, 18, and 19, respectively.

- Include any Rural and/or Urban High Crime Area Job Tax Credits in section 20.

- Report any Other Authorized Credits in section 21.

- Complete the form by signing and dating the declaration that the information is true, under the penalties of perjury. Include your telephone number and, if applicable, the preparer’s signature and telephone number.

After completing all the steps, review the form to ensure accuracy. Attach a check or money order for the amount due, if applicable, and mail it to the Florida Department of Revenue address provided on the form. Filing your sales tax return on time helps avoid any potential penalties or interest for late submissions. If you have any questions or need further assistance, the Florida Department of Revenue websites and support lines are available to guide you through the process.

Understanding Florida Sales Tax

How do I determine taxable sales for the Florida Sales and Use Tax Return?

To determine taxable sales, you must first calculate your gross sales, then subtract any exempt sales to find the taxable amount (line 3). Taxable sales include sales/services (line A), taxable purchases that include use tax on internet or out-of-state untaxed purchases (line B), commercial rentals (line C), transient rentals (line D), and food & beverage vending (line E). Ensure all taxable amounts and categories are accurately reported to comply with Florida law.

What is the Discretionary Sales Surtax and how do I calculate it?

The Discretionary Sales Surtax is a county-imposed tax on most transactions that are subject to the state sales and use tax. Dealers must collect and remit this surtax for taxable sales delivered or used in a county that imposes the surtax. Rates vary by county. To calculate it, use the form DR-15DSS or check online to find your county's rate. Then apply this rate to taxable sales that are subject to the surtax, ensuring to separate exempt amounts for items over $5,000 and reporting the total collected surtax accordingly.

Who needs to complete the Florida Sales and Use Tax Return?

This return must be completed by businesses and individuals that sell taxable goods or services, lease tangible personal property, or operate accommodations or vending machines in Florida. If you are a retailer, wholesaler, or service provider conducting taxable activities, you are required to file this return to report sales and use tax, including any discretionary sales surtax collected.

How do I report exempt sales on the return?

Exempt sales should be reported on line 2 of the return. These include sales that are not subject to sales tax under Florida law. It's important to carefully review the exemptions provided by the Florida Department of Revenue to ensure accuracy in reporting. Documentation supporting the exemption may be required, so maintaining detailed records is crucial.

What are the penalties for not complying with the sales tax return requirements?

Failure to comply, including late filing or payment, fraudulent claims, or evasion of sales tax, can result in penalties. The Florida Department of Revenue imposes specific penalties for these offenses that may include fines and, in severe cases, legal action. Detailed information regarding penalties and fines can be found in the instructions of the Florida Sales and Use Tax Return form or by contacting the Department directly.

Common mistakes

Filing taxes can be daunting, and the Florida Sales Tax form is no exception. Mistakes can lead to penalties, delays, and unnecessary stress. Here are ten common errors people make when filling out the Florida Sales Tax Form (DR-15CS) that can be avoided with a little attention to detail:

- Not including gross sales: Many filers forget to report their gross sales in Line 1. This oversight can skew the entire return, as all subsequent calculations are based on this figure.

- Omitting exempt sales: Line 2 asks for exempt sales, which should be deducted from the gross sales. Failure to report them accurately can result in overpaying taxes.

- Miscalculating taxable amount: The taxable amount in Line 3 is the difference between gross sales and exempt sales. Incorrect calculations here impact the tax liability.

- Forgetting to report use tax: Taxable purchases that have not been taxed appropriately at the time of purchase, especially from out-of-state, need to be reported. Missing this can lead to underreporting taxes due.

- Incorrect transient rental rate or surtax rate: These rates can vary by location, and using outdated or incorrect rates affects the total tax collected.

- Skipping lawful deductions: Line 6 allows for lawful deductions. Not taking advantage of these where applicable can unnecessarily increase the tax due.

- Not deducting the collection allowance: If eligible, filers can deduct a collection allowance. Missing this step leads to an overestimation of the tax due.

- Incorrectly calculating penalties and interest: For late submissions, correctly calculating penalties and interest is crucial. Errors in these calculations can compound the undue financial burden.

- Electronic payment ticking error: For those who pay electronically and fail to indicate this on the form, confusion and processing delays may arise with the Department of Revenue.

- Missing signatures and dates: The Florida Department of Revenue requires both the taxpayer’s and preparer’s signatures along with the date. Not providing these can result in the return being considered incomplete.

It’s important for filers to take their time, double-check their figures, and ensure all required information is accurately provided to avoid these common pitfalls. Remember, when in doubt, consulting the instructions provided by the Florida Department of Revenue or seeking professional assistance can help clarify any confusion and simplify the process.

Documents used along the form

Filing taxes, especially when it comes to sales and use taxes in Florida, requires accurate documentation and a detailed understanding of the process. Alongside the primary Florida Sales Tax Form, DR-15CS, businesses and individuals may need to complete and submit additional forms and documents to comply fully with the state's tax regulations. These documents ensure a comprehensive approach to tax filing, avoiding potential errors that could lead to penalties or audits.

- Application for Certificate of Registration (Form DR-1): Before conducting business in Florida, entities must register with the Florida Department of Revenue. This form is the initial application that allows businesses to collect and remit sales and use taxes, essentially granting them the authority to operate within the state's legal framework.

- Florida Annual Resale Certificate for Sales Tax (Form DR-13): This certificate permits businesses to buy goods tax-free, intending to resell them. It is a crucial document for wholesalers and retailers that purchase products for resale. The annual certificate helps in avoiding the double taxation of goods, ensuring that sales tax is collected only at the final point of sale.

- Discretionary Sales Surtax Information (Form DR-15DSS): Given that many Florida counties impose additional surtaxes on transactions, this form provides updated rates and information on discretionary sales surtaxes. For accurate tax collection and remittance, businesses must stay informed about the surtax rates specific to their county of operation.

- Commercial Rental Sales Tax Return (Form DR-15SW): Businesses that lease or rent commercial property in Florida are subject to sales tax on rental payments. This form is used to report and pay taxes collected from tenants. It includes specific lines for reporting not just the base rental amounts, but also any additional charges that are considered part of the rent under Florida law.

Together with the primary Sales and Use Tax Return, DR-15CS, these documents form a comprehensive toolkit for managing sales tax obligations in Florida. Proper completion and timely submission of these documents not only ensure compliance with state tax laws but also help businesses manage their tax liabilities effectively. It’s important for businesses operating in Florida to familiarize themselves with each of these forms and understand their specific filing requirements to maintain good standing with the Florida Department of Revenue.

Similar forms

The Income Tax Return form is similar because both require the reporting of financial activities to tax authorities, calculating tax payable or refundable, and including deductions and credits.

The Employer's Quarterly Federal Tax Return (Form 941) shares similarities as it involves reporting gross wages, calculating taxes owed, and detailing tax payments made during the quarter.

The State Unemployment Tax forms, filed with state agencies, resemble the Florida Sales Tax form in their requirement for businesses to report earnings and calculate taxes due for state unemployment funds.

Business Property Tax forms, used for reporting the value of business-owned property, are akin to reporting taxable sales and calculating taxes based on property assessments.

The Excise Tax Returns on specific goods and services, such as alcohol, tobacco, and fuel, resemble the Florida Sales Tax form by requiring detailed reports on quantities sold and taxes collected.

Franchise Tax Reports, required by some states from entities doing business within their jurisdiction, are similar as they also calculate tax based on various factors including sales, property, and payroll.

The Use Tax Return for out-of-state purchases not taxed at the point of sale is similar in that it involves self-reporting tax due on items or services used, consumed, or stored.

Value Added Tax (VAT) Returns, applicable in many countries, share the characteristic of documenting sales and purchases through the supply chain, calculating the tax payable to government authorities.

The Customs Duty Declarations for importing goods, which involve declaring the value of goods to calculate taxes and duties owed, have similarities in tax calculation and reporting requirements.

Dos and Don'ts

When it comes to filing the Florida Sales Tax form, it's crucial to approach the process with care and attention to detail to ensure accuracy and compliance. Below are guidelines to help you smoothly navigate filling out this form:

Do's:

- Read the instructions carefully for each line before filling out the form to ensure that each entry is correct and in accordance with the guidelines.

- Double-check mathematical calculations for items such as total taxable sales, discretionary sales surtax collected, and total tax due to prevent errors.

- Ensure that you report exempt sales accurately. This includes understanding which items are exempt and reporting them on the correct line.

- Use the correct surtax rates for your county if applicable, referencing Form DR-15DSS or the provided online resources for accurate rates.

- Sign and date the return. The form is not valid without your signature, attesting to the accuracy of the information provided.

- For electronic payments, mark the appropriate checkbox to inform the Florida Department of Revenue of the payment method.

Don'ts:

- Ignore the bracket system for calculating tax on partial dollar amounts. This can lead to underpaying or overpaying your tax.

- Avoid guessing or estimating figures. Make sure all entries are based on accurate records of your sales and purchases.

- Do not leave any required fields blank. If a particular section does not apply, ensure to mark it as $0 or N/A as appropriate.

- Overlook the discretionary sales surtax. This surtax applies to most transactions and varies by county. Failing to apply the correct surtax can result in discrepancies.

- Omit authorized credits such as enterprise zone jobs credits, which can reduce your total tax due. Ensure to claim all eligible credits accurately.

- Finally, procrastinate on the filing. Late filings can result in penalties and interest charges. Note the due date and make sure your form and payment are submitted on time.

By following these guidelines, you can help ensure your Florida Sales Tax form is filled out accurately and in compliance with state tax regulations, potentially avoiding common pitfalls and mistakes.

Misconceptions

Understanding the Florida Sales and Use Tax Return can often lead to confusion due to prevalent misconceptions. Here are five common misunderstandings:

- Gross Sales are Not Always Taxable in Full: Many assume that the figure entered in the Gross Sales section of the return should be taxed in its entirety. However, this is not always the case, as Gross Sales include both taxable and non-taxable sales. The actual taxable amount is determined after subtracting exempt sales.

- Exempt Sales Need Documentation: Some believe that marking sales as exempt does not require further action. This is incorrect; for sales to be considered exempt, proper documentation must be maintained to justify the exemption, such as resale certificates for items purchased for resale.

- Use Tax Misconceptions: There's a common belief that use tax applies only to tangible goods purchased from out-of-state vendors. However, use tax also applies to taxable services acquired from outside Florida where sales tax was not previously collected.

- Not All Counties Have the Same Surtax Rate: There is a misconception that the discretionary sales surtax is uniform across the state. In reality, surtax rates vary by county, affecting the total tax collected on sales delivered or used within those jurisdictions.

- Penalties for Late Filing Are Automatically Imposed: While penalties can be imposed for late submissions, many don't realize that the Florida Department of Revenue may offer leniency for first-time offenses or under special circumstances, allowing for penalty waivers if the taxpayer meets certain criteria.

It is crucial for businesses operating in Florida to familiarize themselves with the specific requirements of completing the Sales and Use Tax Return accurately to avoid common pitfalls and ensure compliance with state tax laws. By doing so, businesses can better navigate the nuances of tax collection, exemption documentation, and the implications of local surtax variations.

Key takeaways

Filling out and using the Florida Sales Tax form, officially known as DR-15CS, involves several critical steps and considerations to ensure accurate reporting and compliance with state tax laws. Here are key takeaways that taxpayers should be aware of:

- Gross Sales and Exemptions: The form requires you to report gross sales, which encompass all revenue from sales and services before any deductions. Following this, exempt sales must be identified; these are sales not subject to tax under Florida law, which need to be meticulously recorded to ensure accurate calculation of taxable amount.

- Understanding Taxable Amounts: Taxable amounts are derived after exempt sales are subtracted from gross sales. This figure is crucial as it represents the base upon which sales tax is calculated. Additionally, the form requires detailed breakdowns, such as sales/services, taxable purchases, and various types of rentals and vending, highlighting the need for meticulous record-keeping.

- Accurate Calculation of Tax: The form instructs on including use tax on internet and out-of-state untaxed purchases, emphasizing the responsibility to report online purchases that were not taxed at the point of sale. Accurate tax calculation also involves applying the correct transient rental rate and surtax rate, as applicable.

- Discretionary Sales Surtax: Most Florida counties impose an additional surtax, the rates of which vary by county. The form provides a section for reporting surtax collected, underlining the necessity to apply appropriate county surtax rates when calculating total tax duty. It is advisable to consult the latest surtax information to ensure compliance.

- Collection Allowance and Donations: The form offers an option to donate the collection allowance to education, thereby incentivizing timely filing and payment by allowing taxpayers to support local education initiatives directly. Understanding how to properly elect this option can benefit both the taxpayer and the community.

- Late Fees and Penalties: Penalties for late filing or payment, including interest, are clearly delineated on the form. These can accumulate quickly and represent a significant cost, highlighting the importance of understanding the deadlines and potential consequences of delinquency.

- Fraud Penalties: There are severe penalties for fraud, including fraudulent claim of exemption or attempting to evade sales tax. This section of the form and accompanying instructions signify the rigorous enforcement posture of the Florida Department of Revenue and the serious nature of accurate and truthful tax reporting.

While the list above covers essential aspects, the form also contains provisions for dealing with less common scenarios, such as taxable sales of specific goods like electric power or energy and dyed diesel fuel, along with considerations for amusement machine revenues and various tax credits. Each line of the form is designed to capture specific types of transactions, reinforcing the need for comprehensive understanding and accurate reporting of all sales activities.

Popular PDF Templates

Form R405-2020 - Tackle Florida's energy conservation compliance confidently with the detailed instructions and requirements provided in Form 402.

Eviction Notice Florida Pdf - Find out about the possibility of prevailing party obtaining attorney's fees in legal actions related to the rental agreement or law.

Are Sellers Disclosures Required in Florida - This form helps Florida sellers share what they know about their home's condition, making sure buyers are informed before they buy.