Official Florida F 706 Template

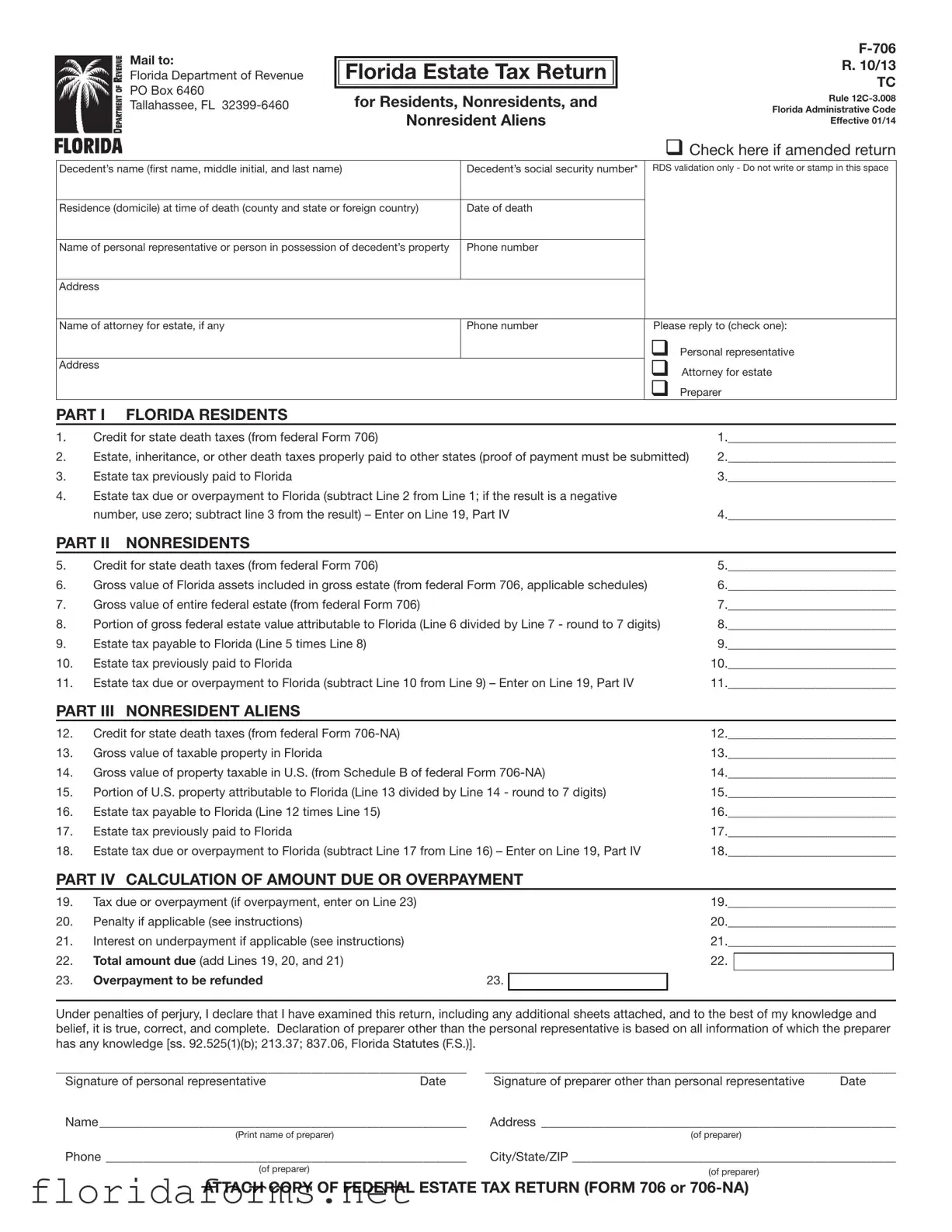

Navigating the complexities of estate taxes in Florida necessitates a thorough understanding of the Florida F-706 Estate Tax Return form, a critical document for executors handling the estates of deceased individuals with ties to Florida, whether as residents, nonresidents, or nonresident aliens. This form serves as a conduit between the estate and the Florida Department of Revenue, providing a structured format for reporting and calculating the estate tax owed to the state, based on the federal estate tax return figures. Integral to this process is the distinction among different categories of filers — Florida residents, nonresidents, and nonresident aliens — each with unique requirements outlined in the form. It includes sections for calculating credits for state death taxes, detailing estate taxes paid to other states, and any previous payments to Florida's estate tax, thereby arriving at the net estate tax due or overpayment to Florida. The form's instructions emphasize the necessity of attaching a copy of the federal estate tax return (Form 706 or Form 706-NA), and delve into specifics about penalties for late payments, interest on underpayments, and the gravitas of filing under the declaration that the information provided is true and complete. For those navigating the estate tax implications in Florida, understanding and accurately completing the F-706 form is paramount to fulfilling legal obligations and ensuring the proper financial closure of the decedent's estate within the state.

Example - Florida F 706 Form

Mail to:

Florida Department of Revenue

PO Box 6460

Tallahassee, FL

|

||

Florida Estate Tax Return |

R. 10/13 |

|

TC |

||

|

||

for Residents, Nonresidents, and |

Rule |

|

Florida Administrative Code |

||

|

||

Nonresident Aliens |

Effective 01/14 |

q Check here if amended return

Decedent’s name (first name, middle initial, and last name) |

Decedent’s social security number* |

RDS validation only - Do not write or stamp in this space |

|

|

|

Residence (domicile) at time of death (county and state or foreign country) |

Date of death |

|

|

|

|

Name of personal representative or person in possession of decedent’s property |

Phone number |

|

|

|

|

Address |

|

|

|

|

|

Name of attorney for estate, if any |

Phone number |

Please reply to (check one): |

|

|

q Personal representative |

Address |

|

q Attorney for estate |

|

|

|

|

|

q Preparer |

PART I FLORIDA RESIDENTS

1. |

Credit for state death taxes (from federal Form 706) |

1.___________________________ |

2. |

Estate, inheritance, or other death taxes properly paid to other states (proof of payment must be submitted) |

2.___________________________ |

3. |

Estate tax previously paid to Florida |

3.___________________________ |

4.Estate tax due or overpayment to Florida (subtract Line 2 from Line 1; if the result is a negative

|

number, use zero; subtract line 3 from the result) – Enter on Line 19, Part IV |

4.___________________________ |

|||||

PART II |

NONRESIDENTS |

|

|

|

|

|

|

5. |

Credit for state death taxes (from federal Form 706) |

|

|

5.___________________________ |

|||

6. |

Gross value of Florida assets included in gross estate (from federal Form 706, applicable schedules) |

6.___________________________ |

|||||

7. |

Gross value of entire federal estate (from federal Form 706) |

|

|

7.___________________________ |

|||

8. |

Portion of gross federal estate value attributable to Florida (Line 6 divided by Line 7 - round to 7 digits) |

8.___________________________ |

|||||

9. |

Estate tax payable to Florida (Line 5 times Line 8) |

|

|

9.___________________________ |

|||

10. |

Estate tax previously paid to Florida |

|

|

10.___________________________ |

|||

11. |

Estate tax due or overpayment to Florida (subtract Line 10 from Line 9) – Enter on Line 19, Part IV |

11.___________________________ |

|||||

PART III |

NONRESIDENT ALIENS |

|

|

|

|

|

|

12. |

Credit for state death taxes (from federal Form |

|

|

12.___________________________ |

|||

13. |

Gross value of taxable property in Florida |

|

|

13.___________________________ |

|||

14. |

Gross value of property taxable in U.S. (from Schedule B of federal Form |

14.___________________________ |

|||||

15. |

Portion of U.S. property attributable to Florida (Line 13 divided by Line 14 - round to 7 digits) |

15.___________________________ |

|||||

16. |

Estate tax payable to Florida (Line 12 times Line 15) |

|

|

16.___________________________ |

|||

17. |

Estate tax previously paid to Florida |

|

|

17.___________________________ |

|||

18. |

Estate tax due or overpayment to Florida (subtract Line 17 from Line 16) – Enter on Line 19, Part IV |

18.___________________________ |

|||||

PART IV CALCULATION OF AMOUNT DUE OR OVERPAYMENT |

|

|

|

||||

19. |

Tax due or overpayment (if overpayment, enter on Line 23) |

|

|

19.___________________________ |

|||

20. |

Penalty if applicable (see instructions) |

|

|

20.___________________________ |

|||

21. |

Interest on underpayment if applicable (see instructions) |

|

|

21.___________________________ |

|||

22. |

Total amount due (add Lines 19, 20, and 21) |

|

|

22. |

|

|

|

|

|

|

|

||||

23. |

Overpayment to be refunded |

23. |

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Under penalties of perjury, I declare that I have examined this return, including any additional sheets attached, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer other than the personal representative is based on all information of which the preparer has any knowledge [ss. 92.525(1)(b); 213.37; 837.06, Florida Statutes (F.S.)].

__________________________________________________________________ |

__________________________________________________________________ |

||

Signature of personal representative |

Date |

Signature of preparer other than personal representative |

Date |

Name___________________________________________________________ |

Address _________________________________________________________ |

||

(Print name of preparer) |

|

(of preparer) |

|

Phone __________________________________________________________ |

City/State/ZIP ____________________________________________________ |

||

(of preparer) |

|

(of preparer) |

|

|

|

|

|

ATTACH COPY OF FEDERAL ESTATE TAX RETURN (FORM 706 or

INSTRUCTIONS FOR FORM

R.10/13 Page 2

General Information

Florida’s estate tax is based on the allowable federal credit for state death taxes. Florida tax is imposed only on those estates subject to federal estate tax filing requirements and entitled to a credit for state death taxes (Chapter 198, F.S.). Estate tax is not due if a federal estate tax return (Form 706 or

Form

The requirement to file Form

Date of Death |

|

|

|

On or before December 31, 2004 |

Yes** |

|

|

On or after January 1, 2005 |

No |

|

|

**If required, Form

Due Dates and Extensions of Time

Form

us within 30 days of mailing the request and 30 days of receiving the federal approval. An extension of time to file does not extend the time to pay. Interest accrues on the Florida tax due from the original due date until paid.

Tax Paid to Other States

For Florida residents: if estate, inheritance, or other death taxes were properly paid to other states, proof of payment must be submitted to the Florida Department of Revenue. (Proof of payment means the final certificate of payment showing the specific amounts of tax, penalty, or interest assessed and paid.)

*Social Security Numbers

Social security numbers (SSNs) are used by the Florida Department of Revenue as unique identifiers for the administration of Florida’s taxes. SSNs obtained for tax administration purposes are confidential under sections 213.053 and 119.071, Florida Statutes, and not subject to disclosure as public records. Collection of your SSN is authorized under state and federal law. Visit our Internet

site at floridarevenue.com and select “Privacy Notice” for more information regarding the state and federal law governing the collection, use, or release of SSNs, including authorized exceptions.

Where to File

Mail your completed

Tallahassee, FL

If you are requesting a nontaxable certificate, include the $5.00 fee.

Signature

The personal representative must sign the return declaration under penalties of perjury. If someone else prepares the return, the preparer must also sign the return.

Amending Form

If you must change a return that has already been filed, you must complete another Form

Penalties and Interest

Penalties – If tax is not paid by the due date (or approved extension date) a late payment penalty of 10% of the unpaid tax is due. After 30 days, the late penalty increases to 20%. An added penalty of 10% per month up to a maximum of 50% of the tax due is imposed if the unpaid tax is due to negligence or intentional disregard. A fraud penalty of 100% of the tax due is imposed if the unpaid tax is due to willful intent to defraud. However, the Department of Revenue is authorized to compromise or settle these penalties pursuant to section 213.21, F.S.

Interest – Interest is due on late payments from the due date until paid. Interest rates are updated January 1 and July 1 of each year. To obtain current interest rates, visit our website at floridarevenue.com.

Need Assistance?

Information and forms are available on our Internet site at

floridarevenue.com.

If you have any questions, you may contact Taxpayer Services at

For a written reply to your tax questions, write:

Taxpayer Services MS

Florida Department of Revenue

5050 W Tennessee St

Tallahassee, FL

For federal estate tax information or forms, visit the IRS website at www.irs.gov.

File Specifications

| Fact Name | Description |

|---|---|

| Governing Law | The Florida F-706 form is governed by Chapter 198, Florida Statutes (F.S.), and Rule 12C-3.008, Florida Administrative Code. |

| Eligibility for Filing | Form F-706 must be filed for estates of Florida residents, nonresidents, and nonresident aliens with Florida property that are required to file a federal estate tax return (Form 706 or Form 706-NA) for dates of death on or before December 31, 2004. After January 1, 2005, the form is not required unless the federal estate tax filing necessitates it. |

| Filing and Payment Deadline | The F-706 form and any payment due must be submitted within 9 months after the decedent's death, coinciding with the federal estate tax return deadline. |

| Amendment Process | If an amendment to Form F-706 is necessary due to changes in the federal Form 706 or 706-NA, a new Form F-706 must be completed with the "amended return" box checked, accompanied by a statement explaining the reasons for the amendment and all related documents. |

Instructions on Filling in Florida F 706

Filing the Florida F-706 Estate Tax Return is an important process for the personal representative or executor of a deceased person's estate. This document is necessary for reporting the estate's tax obligations to the Florida Department of Revenue. It's critical to provide accurate information to ensure compliance with state laws and avoid possible penalties. Below are the steps to properly complete and submit the Florida F-706 form.

- Begin by gathering all necessary documents, including the decedent's federal estate tax return (Form 706 or 706-NA), which must be attached to the Florida return.

- Fill in the decedent's name, social security number, domicile at the time of death, and date of death at the top of the form.

- Indicate whether this is an amended return by checking the appropriate box.

- Enter the contact information for the decedent's personal representative, attorney (if applicable), and the preparer of the return.

- In Part I (Florida Residents), enter the credit for state death taxes from the federal Form 706, any estate taxes paid to other states (with proof of payment), and any estate tax previously paid to Florida. Calculate the estate tax due or overpayment to Florida as instructed.

- In Part II (Nonresidents), fill out the section similarly using values appropriate for nonresidents, including the gross value of Florida assets and the calculation of estate tax payable to Florida.

- For nonresident aliens (Part III), provide the credit for state death taxes from Form 706-NA and relevant values for property in Florida and the overall estate. Then, calculate the estate tax due.

- In Part IV, calculate the total amount due or overpayment, incorporating any penalties or interest if applicable.

- Review all entries for accuracy, ensuring the calculated taxes due and overpayment are correctly entered and all required attachments, including the federal estate tax return, are included.

- The personal representative must sign the form under penalties of perjury. If a preparer other than the personal representative is involved, they must also sign and provide their contact information.

- Mail the completed Form F-706 with the attached federal estate tax return and any other required documents, along with payment if tax is due, to: Florida Department of Revenue PO Box 6460 Tallahassee, FL 32399-6460

- If requesting a nontaxable certificate, include the necessary $5.00 fee with your submission.

After submitting the Form F-706, it is advisable to keep a copy of all documents for your records. In the event of discrepancies or questions from the Florida Department of Revenue, having detailed records will facilitate clarifications or corrections. Adherence to deadlines is crucial to avoid penalties or interest on late payments. Should there be a need to amend a previously filed F-706 form, remember to check the amended return box and attach a statement explaining the changes alongside the amended federal return.

Understanding Florida F 706

What is the Florida F-706 Form?

The Florida F-706 Form, or Florida Estate Tax Return, is a document used to calculate and report the estate tax due to the state of Florida. It is required for estates of Florida residents, nonresidents, and nonresident aliens with property in Florida that meet federal estate tax filing requirements. The form calculates tax based on allowable federal credits for state death taxes.

Who needs to file the Florida F-706 Form?

Form F-706 must be filed for the estate of every Florida resident, nonresident, and nonresident alien who has Florida property and is required to file a federal estate tax return (Form 706 or Form 706-NA). If the decedent's date of death is on or before December 31, 2004, the form is required. For dates of death on or after January 1, 2005, filing is not necessary.

When is the Florida F-706 Form due?

The Florida F-706 and any payment due are required within 9 months after the decedent’s death. This coincides with the federal estate tax return due date. If an extension is needed, requests should be made to the IRS, as Florida will grant the same extension for both file and payment if approved federally. However, interest on any due tax will accrue from the original due date until payment is made.

What if tax was paid to other states?

For Florida residents who have paid estate, inheritance, or other death taxes to other states, proof of payment must be submitted to the Florida Department of Revenue with the F-706 form. This proof must include the final certificate of payment that shows the specific amounts of tax, penalty, or interest assessed and paid to the other state.

How do I submit an amended Florida F-706 Form?

If a return already filed needs to be amended, a new Form F-706 should be completed with the amended return box checked. An amended return might be necessary due to changes in the federal Form 706 or 706-NA. It should be accompanied by a statement describing the reasons for the amendment and all related documents, including any correspondence from the IRS or the amended federal form.

What penalties and interest apply for filing or paying late?

Late payments incur a penalty of 10% of the unpaid tax if not paid by the due date or approved extension date. This penalty increases to 20% after 30 days and may include an additional penalty of 10% per month up to a maximum of 50% of the tax due for negligence or intentional disregard. Fraudulent actions can incur a penalty of 100% of the tax due. However, penalties may be settled or compromised by the Department of Revenue.

Where can I find assistance or more information?

For more guidance and access to forms, visit the Florida Department of Revenue's website at floridarevenue.com. If you have specific questions or need direct assistance, you can contact Taxpayer Services at 850-488-6800, Monday through Friday, excluding holidays. For federal estate tax information or forms, the IRS website at www.irs.gov is a valuable resource.

Common mistakes

When it comes to navigating the complexity of filling out the Florida F 706 form, several common mistakes can lead to unnecessary headaches and potentially costly errors. Understanding these pitfalls is crucial for ensuring the accurate and timely processing of an estate tax return. Here's an overview of six common mistakes people make:

Not attaching a copy of the federal estate tax return: Filing the Florida F 706 form requires attaching a signed copy of the federal estate tax return, either Form 706 or Form 706-NA, depending on the decedent's status. Overlooking this step can result in processing delays.

Incorrect calculation of the estate tax: Properly calculating the estate tax due to Florida involves accurately completing several sections of the form, depending on whether the estate is for a resident, nonresident, or nonresident alien. Misinterpretations in calculating these values can lead to incorrect tax amounts being reported.

Failing to submit proof of payment for taxes paid to other states: For Florida residents, if estate taxes have been paid to another state, proof of such payments must be submitted along with the F 706 form. Neglecting to include this documentation can hinder the determination of any credit due for taxes paid elsewhere.

Omission of the Social Security Number (SSN): The decedent’s SSN is a critical piece of information used for identification purposes. Failing to provide this detail can lead to delays and issues in processing the return.

Not requesting an extension properly: If more time is needed to file the form or pay the tax due, it's necessary to request an extension from the IRS. However, a copy of the extension request and the IRS's approval must be sent to the Florida Department of Revenue within the specified timeframe. Missing these steps can lead to penalties.

Inaccurately reporting the decedent's residence: The form requires the decedent's residence (domicile) at the time of death to be listed accurately. A mistake here can affect the determination of the estate's tax liability to Florida.

Steering clear of these common errors can make the process of completing the Florida F 706 form smoother and can help ensure that the estate's financial affairs are in good order.

Documents used along the form

When dealing with the complexities surrounding the Florida F-706, Estate Tax Return, it's crucial to recognize that this form does not exist in isolation. Several additional forms and documents often accompany the F-706 to ensure compliance with estate planning, tax obligations, and administrative requirements. Each of these documents plays a unique role in the estate settlement process, serving to streamline the handling of the decedent’s estate, detail asset distributions, and fulfill both state and federal tax duties.

- Federal Estate Tax Return (Form 706 or 706-NA): Required attachment for the Florida F-706, providing detailed information on the decedent's estate assets and their values for federal tax purposes.

- Affidavit of No Florida Estate Tax Due (Form DR-312): For estates not required to file a federal estate tax return, this affidavit helps release the Florida estate tax lien on the property.

- Application for Extension of Time to File (IRS Form 4768): Required when seeking an extension for filing the estate’s federal tax return, which indirectly affects the filing deadline for the F-706.

- Certificate of Payment from Other States: Provides proof of death taxes paid to other states, necessary for Florida residents claiming a credit on the F-706.

- Consent to Transfer (Federal Form 712): Used when transferring life insurance or other property for which the estate seeks a release of federal tax lien before the estate taxes are fully settled.

- Florida Probate Documents: Including the death certificate, wills, and trust documents, these are essential for establishing the legal context of the estate.

- Statement Regarding Amended Federal Return: If the federal estate tax return (Form 706 or 706-NA) is amended, a descriptive statement and documents related to the changes must accompany the amended F-706.

- Inventory of Estate Assets: While this internal document may not always be formally submitted, it's critical for accurately completing the Florida F-706 and its federal counterpart.

- Power of Attorney (Form DR-835): Allows a designated individual to act on behalf of the estate in tax matters with the Florida Department of Revenue.

- Release of Lien Certificate: Issued by the Florida Department of Revenue upon full settlement of the estate's tax liabilities, releasing any liens on the estate’s assets.

The interplay between these documents and the Florida F-706 form underscores the importance of meticulous preparation and understanding of the estate's obligations. It's vital not only to complete each form with accuracy but also to appreciate how they collectively facilitate the estate's navigation through Florida’s tax requirements. Whether finalizing tax payments, transferring assets, or officially closing the estate, each document contributes to achieving compliance and securing the decedent's legacy.

Similar forms

The Federal Form 706 or the United States Estate (and Generation-Skipping Transfer) Tax Return is directly comparable to the Florida F-706 form in purpose and structure. Both forms calculate estate tax obligations, but while the Federal Form 706 focuses on the entire estate irrespective of location, the Florida F-706 specifically calculates taxes due for estates with ties to Florida - whether the individuals were residents, nonresidents, or nonresident aliens.

Federal Form 706-NA, the United States Estate (and Generation-Skipping Transfer) Tax Return for Nonresident not a Citizen of the United States, shares similarities with the Florida F-706 in its approach to nonresident aliens. Both documents require information on assets within their respective jurisdictions and cater to the specific tax obligations of nonresidents or nonresident aliens.

Florida Form DR-312, Affidavit of No Florida Estate Tax Due, is designed for estates not required to file a federal estate tax return and thereby not liable for Florida estate tax. This form is similar to the F-706 in that it deals with the determination of estate tax liability in Florida, but it caters to estates that are exempt from these taxes.

The New York State Estate Tax Return (ET-706) parallels the Florida F-706 form because both are state-specific estate tax forms that determine estate tax liability based on the value of the estate's assets within the state. They both accommodate residents and nonresidents, adjusting calculations based on the location and value of assets.

California Estate Tax Return, while not required for most estates due to changes in state laws, when applicable, served a similar purpose as the Florida F-706. It was used to calculate state-specific estate taxes owed based on federal estate tax calculations.

Illinois Form 700, the Illinois Estate and Generation-Skipping Transfer Tax Return, serves a role similar to the Florida F-706 form by determining estate tax due to the state. It adjusts tax obligations based on credits from state death taxes and mirrors the requirement for estates to be subject to federal estate tax filings.

Pennsylvania Inheritance Tax Return shares common ground with Florida's F-706, as both are concerned with taxes arising from the transfer of assets at death. Despite differences in tax nomenclature and calculations (inheritance vs. estate tax), the core purpose aligns in addressing state-level tax obligations post-mortem.

New Jersey Estate Tax Return closely resembles the F-706 structure by serving residents and nonresidents who own property within the state. It requires detailed listings of in-state property to calculate state estate taxes, similarly leveraging federal estate tax data for its basis.

Oregon Estate Transfer Tax Return aligns with the Florida F-706's objectives by assessing state taxes on estates that have a federal filing requirement. Although specific tax rates and exemptions differ, the overall premise of leveraging federal estate tax determinations to impose a state-level obligation is a shared characteristic.

Dos and Don'ts

When managing the complexities of the Florida F-706 Estate Tax Return, individuals tasked with closing the estate of a deceased person face a delicate balance. This document, a critical step in adhering to both state and federal tax obligations, requires careful attention to detail and adherence to regulatory guidelines. Here are some do's and don'ts that should be considered:

- Do carefully review the instructions provided by the Florida Department of Revenue. These instructions offer a roadmap for completing the form accurately and are tailored to the unique aspects of Florida estate tax law.

- Do check the box for an amended return if you are making changes to a F-706 form that was previously filed. This ensures clarity and compliance in the amendment process.

- Do attach a copy of the federal estate tax return (Form 706 or 706-NA) as required. This connection between federal and state tax documents is critical for a cohesive tax strategy.

- Do provide the decedent’s social security number. This serves as a unique identifier that is essential for the processing and administration of the estate’s tax obligations.

- Do ensure that the tax due or overpayment is calculated accurately in Part IV and that any penalties or interest owed are accounted for.

- Don’t overlook the necessity of checking whether an estate tax return needs to be filed based on the date of death. The requirements have evolved over time.

- Don’t disregard the deadline for filing and paying the estate tax, which is within nine months after the decedent's death. Late filings can result in penalties and interest.

- Don’t neglect to request an extension from the IRS if more time is needed for filing or paying, remembering to send copies of the extension request and approval to the Florida Department of Revenue within the specified time frames.

- Don’t forget to sign the return. A personal representative’s signature verifies the accuracy and completeness of the return under the penalties of perjury. If another person prepares the return, that individual must also sign and provide their details.

It is essential for personal representatives to approach the Florida F-706 form with diligence. The completion and filing of this document not only fulfill a legal duty but also honor the financial legacy of the decedent. By following these guidelines, filers can navigate the process more effectively, ensuring compliance and contributing to a smooth transition during a challenging time.

Misconceptions

When dealing with the Florida F-706 form, it's vital to approach it with a clear understanding. Below are seven common misconceptions that need to be clarified:

- Only for Florida Residents: It's a common mistake to think the F-706 is only for Florida residents. In truth, this form is for residents, nonresidents, and nonresident aliens with property in Florida.

- No Longer Required: Some believe that the F-706 form is no longer required due to changes in state law. However, for dates of death on or before December 31, 2004, this form remains a requirement if a federal estate tax return is necessary.

- Duplicate Extensions: There's a misconception that separate extension forms must be filed with the Florida Department of Revenue and the IRS. Florida recognizes federal extensions, but you must send copies of these extensions to the Florida Department of Revenue.

- Automatic Penalties: The belief that penalties are automatic and non-negotiable can be misleading. The truth is that penalties for late payment can be compromised or settled under certain Florida statutes.

- Social Security Numbers Are Optional: Some might think providing a social security number on this form is optional. However, these numbers are crucial for tax administration and are kept confidential, based on state and federal laws.

- Filing Location Confusion: There’s often confusion about where to file the F-706. All completed forms and payments should be directed to the specified Florida Department of Revenue address in Tallahassee, FL.

- Overpayments Are Automatically Refunded: Finally, there’s a misconception that any overpayment will automatically be refunded, but you need to accurately report and calculate overpayments on the form to ensure proper processing.

Understanding these points can help navigate the complexities of the Florida F-706 form more effectively and avoid potential pitfalls in estate tax filing.

Key takeaways

Understanding the intricacies and proper completion of the Florida F-706 form is crucial for the accurate handling of estate taxes within the state. Here are key takeaways to navigate the process effectively:

- Filing Requirement: The need to file Form F-706 depends on the decedent's date of death. For deaths on or before December 31, 2004, filing is required. However, for deaths on or after January 1, 2005, there is no requirement to file this form.

- Attachments: For those estates that are required to file, a signed copy of the federal estate tax return (Form 706 or Form 706-NA) must be attached to the Florida estate tax return.

- Due Dates: The Form F-706 and any payment due must be submitted within 9 months of the decedent’s death. This is aligned with the due date for the federal estate tax return.

- Extensions: If an extension of time to file or pay is necessary, requests should be directed to the Internal Revenue Service (IRS). Florida will honor the same extension granted by the IRS, provided that proof of the federal extension is forwarded to the Florida Department of Revenue within the specified timeframe.

- Interest and Penalties: Late payments are subject to both interest charges and penalties. Interest accrues from the original due date until the tax is paid. Penalties can range from 10% to 100% of the unpaid tax, depending on the cause and duration of the delay.

- Tax Paid to Other States: For Florida residents, estate taxes paid to other states must be documented and proof submitted with Form F-706 to be eligible for any applicable credits or deductions.

- Social Security Numbers: SSNs are required on the form for tax administration purposes and are kept confidential in accordance with state and federal law.

- Where to File: Completed forms and payments should be mailed to the Florida Department of Revenue at the specified PO Box in Tallahassee, FL.

- Signature Requirements: The form must be signed by the personal representative under penalties of perjury. If the return is prepared by someone other than the personal representative, that preparer must also sign the form.

- Amending Form F-706: To amend a previously filed return, complete a new F-706 form, check the "amended return" box, and attach any required statements or documents detailing the changes from the original filing.

By adhering to these guidelines, individuals responsible for managing the estate of a deceased Florida resident, nonresident, or nonresident alien can ensure compliance with state tax regulations and avoid unnecessary penalties or interest charges.

Popular PDF Templates

How to Create an Online Job Application - The form asks for consent to conduct background checks as required for certain positions.

Florida Medical License - Parents are encouraged to seek additional vision and dental examinations for their children, as recommended by the Partnership for School Readiness.

Sellers Permit Florida - No signature is required on the certificate, simplifying the process of tax-exempt purchases for resale.